API Holdings PharmEasy Limited

Fundamentals

| PharmEasy Unlisted Shares Price | Rs 6.5 Per Equity Share | Market Cap (in cr.) | Rs 11071 |

| Lot Size | 5000 Shares | P/E Ratio | N/A |

| 52 Week High | Rs 9 | P/B Ratio | 3.39 |

| 52 Week Low | Rs 6.5 | Debt to Equit | 0.62 |

| Depository | NSDL & amp; CDSL | ROE (%) | -48.05 |

| PAN Number | AASCA1201E | Book Value | 1.92 |

| ISIN Number | INE0DJ201029 | Face Value | 1 |

| CIN | U60100MH2019PLC323444 | Total Shares | 17032495304 |

| RTA | Link Intime |

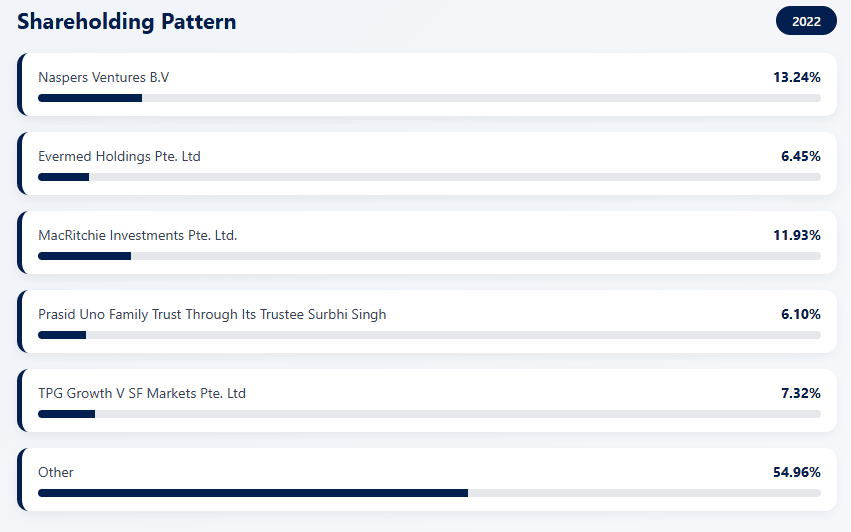

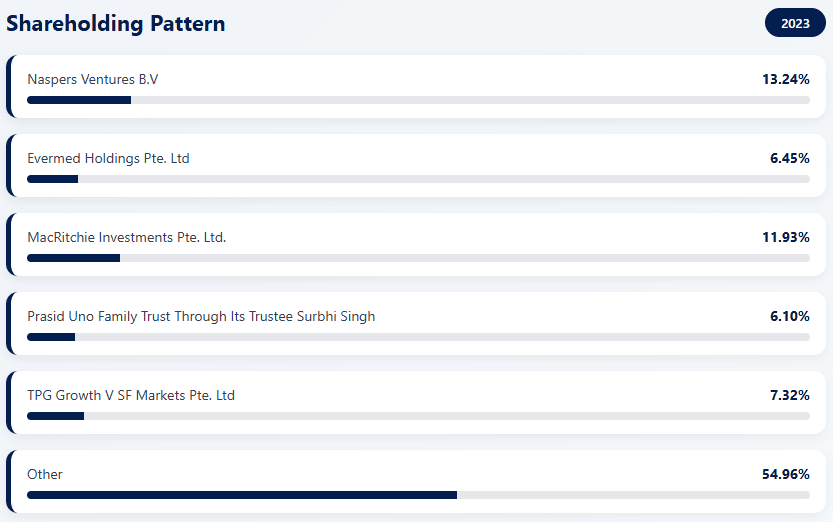

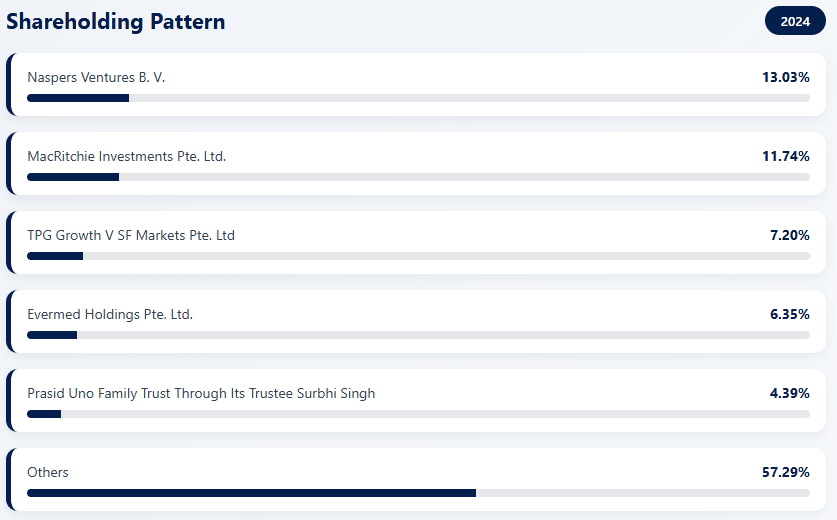

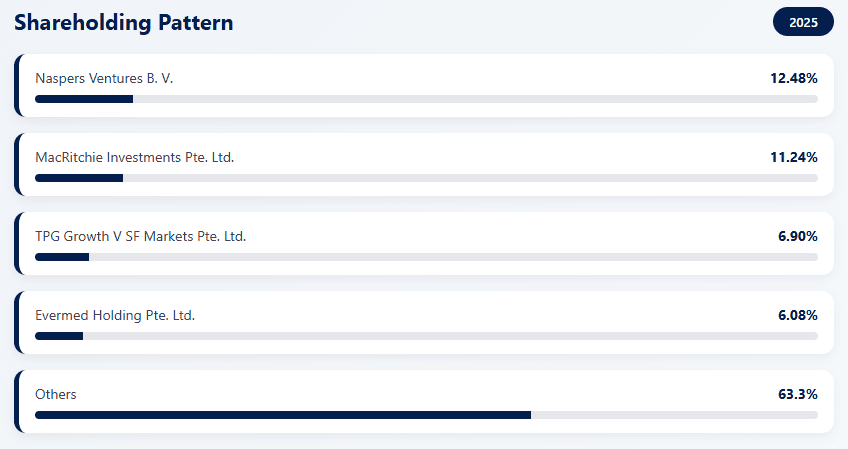

Shareholding Pattern

API Holdings PharmEasy Limited

API Holdings Limited is the Mumbai-based parent company of PharmEasy, India's prominent integrated digital healthcare platform. It operates an end-to-end ecosystem connecting consumers, pharmacies, and diagnostic labs through a sophisticated tech stack that includes B2C e-pharmacy services, large-scale diagnostics via Thyrocare, and B2B supply chain solutions through Retailio and Aknamed.

As of early 2026, the company has pivoted from aggressive expansion to a "turnaround" strategy focused on debt reduction and unit economics. After a significant valuation down-round in 2023, the platform has successfully halved its annual losses to approximately Rs 1,572 crore (FY25) and refinanced its debt through NCDs. While it previously dominated the market, recent data shows it now faces intense competition from Tata 1mg, which holds a lead in market share. Despite these challenges, API Holdings remains a major private player delivering to over 1,000 cities, with ongoing preparations to potentially revisit its IPO in 2026 or 2027.

Company Business Model

API PharmEasy Limited operates a digital healthcare commerce platform that connects consumers with medicines, diagnostics, and healthcare services through a technology-driven, asset-light model.

Online Pharmacy Sales

Generates revenue by selling prescription and OTC medicines directly to consumers via its app and website.

Diagnostics Aggregation

Earns commissions by facilitating lab test bookings through partnered diagnostic providers.

Integrated Supply Chain

Backward integration into pharmaceutical distribution improves margins, availability, and delivery efficiency.

Private Label Products

Sells in-house wellness and healthcare products to enhance profitability.

Competitors

PharmEasy competes with major digital health platforms (Tata 1mg, Apollo 24|7, Netmeds) and omni-channel pharmacy chains, with competition centered on pricing, delivery speed, diagnostics integration, and customer retention.

Tata 1mg

Online pharmacy, diagnostics, and doctor consultations.

Apollo 24|7

Backed by Apollo Hospitals; strong omni-channel presence.

Netmeds

Reliance-backed e-pharmacy with nationwide reach.

Practo

Consultations and diagnostics with pharmacy integration.